As the “convenience is king” retail paradigm continues to influence banking, we are seeing the emergence of a new technology and additional delivery channel that could greatly expand the possibilities of the humble ATM. That technology is the interactive teller machine, or ITM, which physically resembles an ATM but comes complete with a video and audio connection to live tellers in an organization’s call center. Most notably, the number of different transaction types the technology is capable  of is an order of magnitude greater than that of an ATM.

of is an order of magnitude greater than that of an ATM.

We recently spoke with Bryan Woodward, COO at Finex Credit Union, and a pioneer of the ITM in the New England region. Woodward was instrumental in driving an emergent philosophy at Finex (and earlier at Connex) credit union through the adoption of the remote teller model.

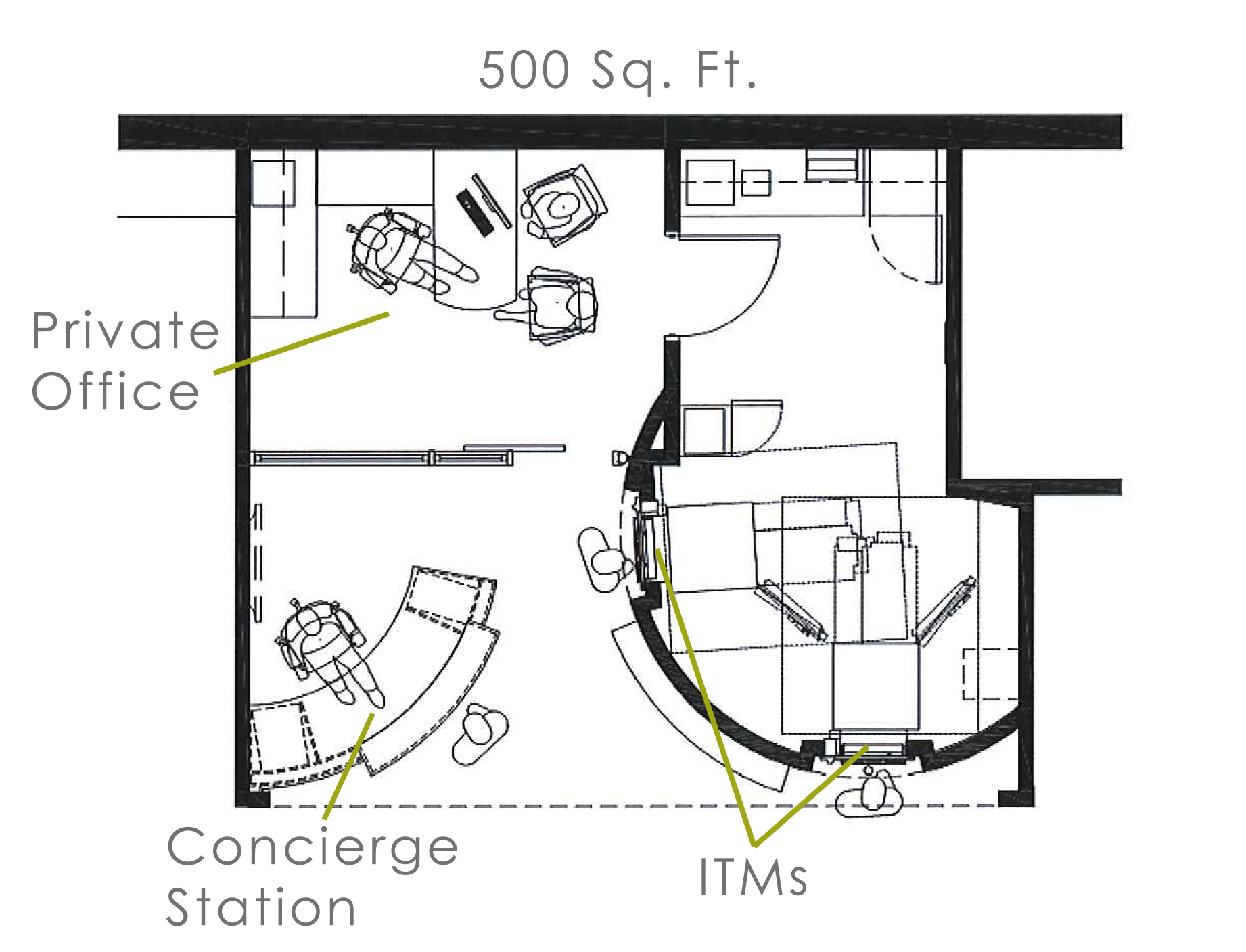

“We began from scratch with the ITMs,” he said. “Design posed some big questions for us initially. From the very beginning, building the right design and shape for the queuing area around the technology tested our creative resources. These questions haven’t gone away today, because each new branch is different,  and the staging for an ITM has to be thought out in advance to avoid what can be quite serious shortcomings with regard to traffic flow. We improved the model each time we implemented a new ITM, always with the flow of branch traffic in mind.”

and the staging for an ITM has to be thought out in advance to avoid what can be quite serious shortcomings with regard to traffic flow. We improved the model each time we implemented a new ITM, always with the flow of branch traffic in mind.”

ITMs seem almost too good to be true. Their versatility means that a broad variety of an organization’s products and services can be offered at all locations, with extended hours. In effect, the smallest microbranch could function much like a full-service hub, but in a more convenient location. That said, member and  customer reaction to the switch from a traditional teller line to interactive teller machines can be mixed.

customer reaction to the switch from a traditional teller line to interactive teller machines can be mixed.

“Preparing properly for member reaction to the new technology is as important as designing the queuing area properly,” Woodward said. “Some members will resist the change. They expect something more traditional, so you have to develop a plan for a ‘hand-holding’ period. Teaching these members how to use the technology is crucial to the success of the ITM.”

Migrating members and customers from a traditional teller line onto an ITM saves money and improves staff efficiencies. Fewer employees are able to service multiple branches from a call center. Those employees are now busier than they would be at a teller line, so productivity is improved while other staff can be trained to perform higher value tasks. Woodward said that the scope of activities conducted at the ITM can be defined and separated from other banking activities, which is a big part of maintaining an orderly queuing area.

“We segment cash transactions at the video teller and any other branch activities are done in a different place in the branch, which keeps the ITM line flowing,” he said. “The remote tellers can service members in any branch, regardless of where that branch is. They’re much more engaged with members as well as being more efficient in the way that they deal with each call.”

Branch In A Box

Some of the benefits of an ITM may not be immediately obvious, but there are many. For instance, if a customer needs to withdraw an amount of cash that exceeds the upper limit of a traditional ATM, the remote teller can authorize this amount as if they were physically present at the branch. Another example is seven-day teller access. This happens when a microbranch with ITMs is located in a supermarket. To be available to the supermarket’s customers, the branch has to be open seven days a week. Tellers must therefore be working at the call center to service those using the ITM. This means members/customers at other branches can also be served by tellers on ITMs and perform a variety of transaction types, including on Sundays.

“To be available for the supermarket’s customers, the microbranch needs to be open seven days a week,” Woodward said. “Those ITMs at all our other branches are therefore open for remote teller access. A video teller in the call center can take calls from all ITMs on the network simultaneously so our customers enjoy teller access every day of the week.”

ITMs are also agile enough to save banks and credit unions money when expanding their networks. The “branch in a box” solution is highly beneficial tool for testing new markets. A bank or credit union can place the ITM in a convenient location on a short lease. If it proves to be successful they can build a branch in that locale, or continue to maintain the ITM there on a permanent basis. If it isn’t successful they can simply move the ITM to a different location. There could be a location where the organization doesn’t want a branch but it’s desirable to maintain a presence in that area with very little real estate. All that’s required are power and data and the ITM can deliver a competitive level of service.

Interactive teller machines were inevitable; the financial industry is coming to terms with technology and it is beginning to use it to save time and money. Basic branch functions such as depositing or withdrawing cash, transferring money between accounts and depositing checks, are the low hanging fruit for freshly implemented ITM networks. These time-consuming but low value activities can be performed quickly and easily on ITMs, while higher trained staff can help members and customers become more engaged with the brand and perform value-added tasks.

Fully-automated branches utilizing greater numbers of transaction types already exist, but they’re set to become the norm over the next decade. These tellerless branches currently require less than half the staff of a traditional branch, and these numbers will become even more efficient as user familiarity and ITM proficiency increases. Expect to see the ITM begin to play a central role in many newly designed branches in the near future.

Ian Hough is director of marketing for Solidus, a Connecticut-based branch design-build firm. He may be reached at ihough@gosolidus.com.