Courtesy photo

Perhaps the only state-chartered bank in Connecticut with a current African American CEO and president is being accused of discriminating against African-American and Latino residential mortgage applicants.

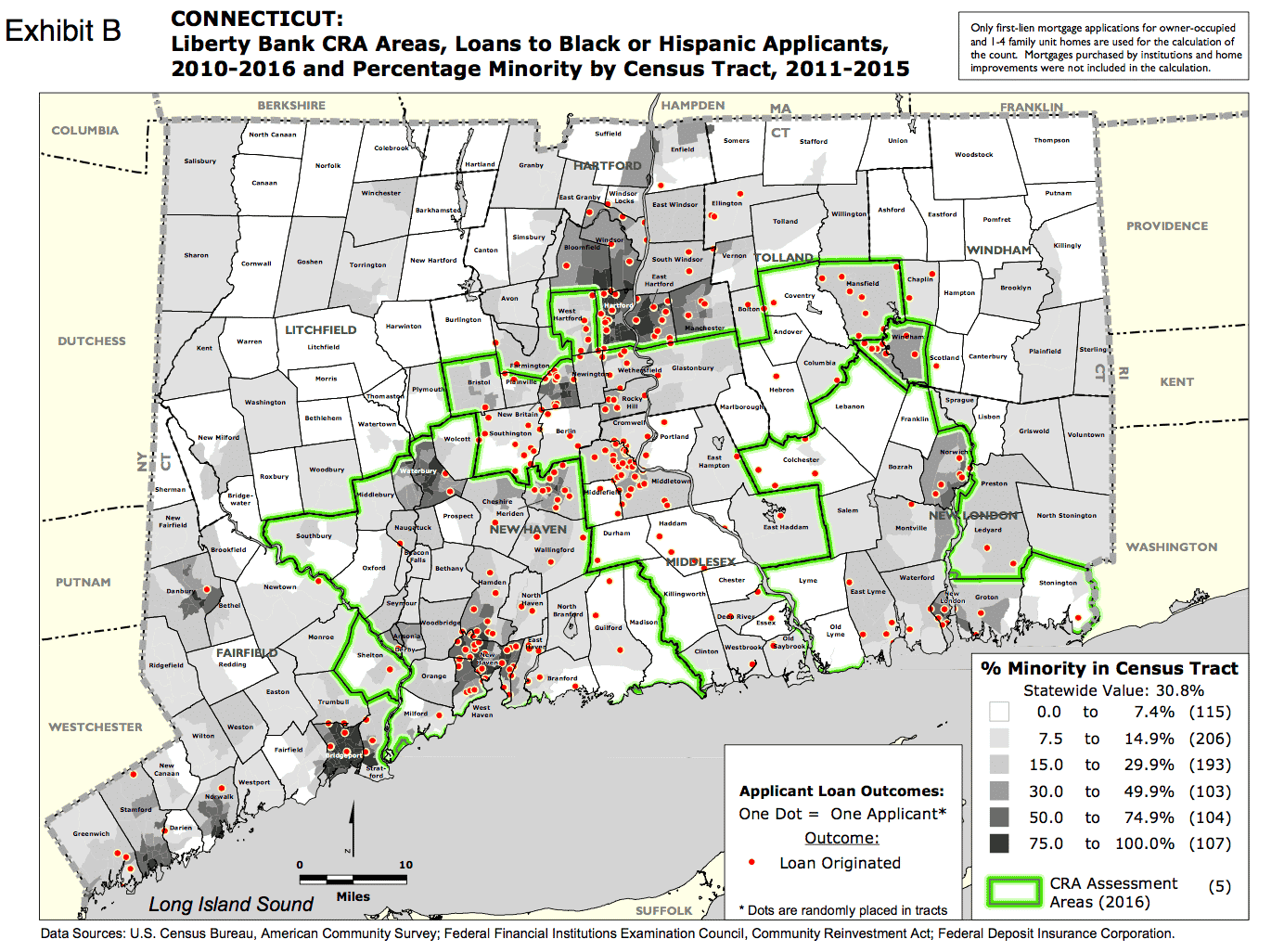

The Connecticut Fair Housing Center earlier this month filed a federal lawsuit against Middletown-based Liberty Bank, alleging the lender violated the Fair Housing Act by “redlining” in communities where most residents are individuals of racial and ethnic minorities.

The lawsuit states that the bank during the application process denied African-American and Latino applications at significantly higher rates than those from white applicants.

“They happen to be the worst [in Connecticut],” Jeff Gentes, managing attorney at the Connecticut Fair Housing Center, told The Commercial Record. “They are not the only one doing badly. We do this publicly, so we can have an effect beyond the one bank we sue.”

The lawsuit alleges that only 3.34 percent of Liberty Bank’s total originations went to African Americans or Latino applicants between the years 2010 and 2016.

Among the top nineteen mortgage lenders in the state, Liberty Bank, which declined to comment, has the widest racial lending disparities in refinance denials for African-American and Latino applicants compared with White applicants.

The bank also failed to provide refinance loans to communities of color at a rate that outstrips its peers at a statistically significant level, the lawsuit alleges.

The Connecticut Fair Housing Center made its findings using data publicly released under the Home Mortgage Disclosure Act, as well as with data from Community Reinvestment Act assessments.

“We didn’t rely on secret data. We relied on data that Liberty puts out there and that Liberty had access to that shows they were redlining,” said Gentes. “There was nothing proprietary on our end.”

The Connecticut Fair Housing Center also conducted testing at six Liberty Bank branches, and as a result, alleges that Liberty loan officers made statements that would discourage a prospective applicant from a protected class from applying for credit.

The center sent African American, Latino and White borrowers to various Liberty branches, all of which were qualified for a 30-year fixed rate or adjustable rate mortgage using the Fannie Mae manual underwriting matrix.

And while the testers had similar credit metrics, the Connecticut Fair Housing Center alleges Liberty Bank loan officers discouraged non-White borrowers from applying for loans and provided less information and offered worse terms to non-White borrowers.

In one test, according to the lawsuit, the same Liberty loan officer offered a White tester a 3 percent down payment and an African-American tester a 5 percent down payment, despite the two having similar credit metrics. During that same test, the lawsuit alleges the loan officer asked for information about the African American borrower’s debt and rent payments that he did not ask from the White borrower.

In other tests, according to the lawsuit, when Latino and African American borrowers requested written mortgage materials, they were told there were none available or to look at some type of down payment assistance program. Conversely, White borrowers were provided with packets of mortgage solutions.

While Liberty Bank may have never failed any of its Community Reinvestment Act exams, the lawsuit alleges this is because the bank has avoided lending in majority non-white areas.

Under CRA, Liberty Bank can draw its own assessment area. The lawsuit alleges that Liberty’s assessment area purposely avoids non-White areas such as Hartford, East Hartford and Manchester.

As a result, of the 2,916 conventional home purchase loans made by Liberty Bank between 2010 and 2016, a little over 10 percent, 294 to be exact, were in diverse census tracts and only 126 were in majority non-white census tracts.

Of the 4,919 refinance loans made during these years, only 6.9 percent were made in diverse census tracts and 1.7 percent were in majority non-white census tracts.

“Fair lending is incidental to CRA assessment and it’s rare that any CRA review leads to some kind of fair housing action,” said Gentes. “It’s no defense to violating the Fair Housing Act.”

Gentes said the Connecticut Fair Housing Center has not yet determined the exact monetary amount it is seeking in damages, but will likely get a better idea as the case gets into discovery.