Waterford-based Charter Oak Credit Union, which operates in a footprint that has a military presence, was a top lender in 2018 for both FHA and VA loans. Image courtesy of Charter Oak Credit Union.

Waterford-based Charter Oak Credit Union, which operates in a footprint that has a military presence, was a top lender in 2018 for both FHA and VA loans. Image courtesy of Charter Oak Credit Union.

Despite a contracting mortgage market, some leading providers of loans guaranteed by the U.S. Department of Veteran Affairs and Federal Housing Administration managed to retain their positions in these categories, according to a new report from The Warren Group, publisher of The Commercial Record.

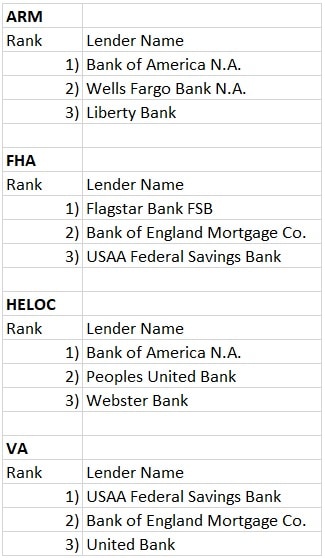

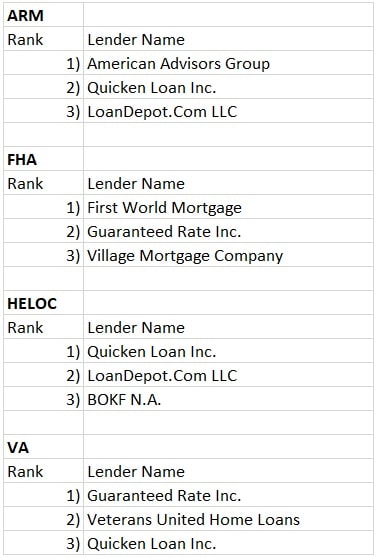

For the first time, The Warren Group is reporting the top lenders of VA and FHA loans in Connecticut in . The rankings include banks, credit unions and mortgage companies.

While different products, both VA and FHA loans typically allow borrowers to put very little money down, or none at all, on a home mortgage. Various government agencies then fill in the gap so banks can originate the mortgage and still meet their underwriting standards.

These loans also allow borrowers to qualify with lower credit scores and offer other advantages, such as using an unsecured loan to cover closing costs. Although both are lenient, VA loans are considered to have the easiest standards to qualify for.

Waterford-based Charter Oak Credit Union, which operates in a footprint that has a military presence, was a top lender in 2018 for both FHA and VA loans.

Despite seeing a slowdown in 2018 due to rate hikes, the credit union was able to stay a top lender in these loan categories through the reputation it has built up over the years, said John Dolan, senior vice president and chief lending officer at Charter Oak.

“We have good marketing presence here and our membership knows us so that’s why we get referral business,” he said. “Usually it’s members talking to other members saying, ‘Go see Charter Oak.’”

Competition Emerges from PMIs

However, as mortgage volume has come down all around, the competition for borrowers has stiffened.

Not only is Charter Oak facing its usual competition from Virginia-based Navy Federal Credit Union, the largest credit union in the country, but private mortgage insurance companies have begun to emerge as rivals, as well.

Conventional borrowers who make less than a 20 percent down payment on a home are required to make a PMI payment each month.

John Dolan

Unlike conventional loans, FHA and VA borrowers are not required to pay for PMI, although they still have premium payments each month.

However, conventional loans are often more advantageous for borrowers who qualify because once a their loan-to-value ratio falls below 78 percent, the PMI payments go away, whereas the premium payments on FHA and VA loans extend through the life of a loan.

But since PMI companies have gotten less business from banks and other financial institutions as overall mortgage volume shrunk in 2018, they have begun to release new products, according to Dolan, that are more flexible and require less money down, making them more similar to the VA and FHA products.

“Overall volume was down 25 percent year-over-year. That means the PMI companies were getting less business from us and therefore get more competitive with each other,” he said. “As PMI gets more creative with their products, that lessens demand for VA and FHA products in our market.”

Banks

Covers residential mortgages only. Ranked by dollar volume of loans.

Source: The Warren Group’s Marketshare Module

Credit Unions

Covers residential mortgages only. Ranked by dollar volume of loans.

Source: The Warren Group’s Marketshare Module

Mortgage Companies

Covers residential mortgages only. Ranked by dollar volume of loans.

Source: The Warren Group’s Marketshare Module