While the economic crisis caused by the coronavirus pandemic saw investors raise some criteria for purchasing these loans on the secondary market, concerns that first-time homebuyers would lose access to these loans have not panned out.

Even with Connecticut’s low inventory of homes for sale, first-time homebuyers found ways into the housing market last year, including with the assistance of government-insured mortgages.

Loans offered through the Federal Housing Administration made up almost 11 percent of Connecticut’s residential purchase mortgages in 2019, according to The Warren Group, publisher of The Commercial Record.

With lower down payment and credit requirements compared to other mortgages, FHA loans have been a key resource for first-time homebuyers. While the economic crisis caused by the coronavirus pandemic saw investors raise some criteria for purchasing these loans on the secondary market, concerns that first-time homebuyers would lose access to these loans have not panned out.

“There was a lot of misconception that FHA was widely unavailable, and that really is not the case,” said Tim Martin, vice president of mortgage lending at Guaranteed Rate Affinity in Westport. “It continues to be a great product for people whose credit is good but not great.”

Key Tool for Many Buyers

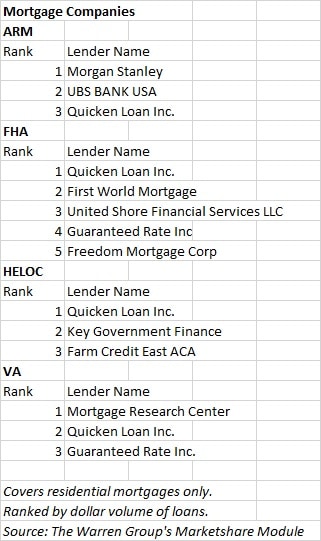

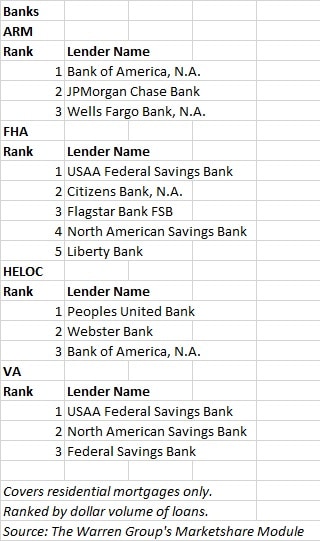

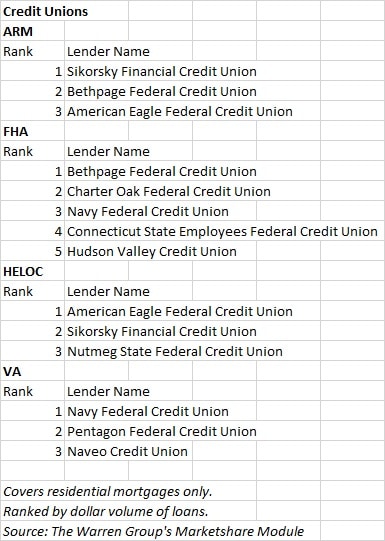

The Warren Group is reporting the top lenders for FHA loans, as well as VA loans, home equity lines of credit and adjustable-rate mortgages in Connecticut. The rankings include banks, credit unions and mortgage companies and are based on loan volume in 2019.

Used to purchase a primary residence, FHA loans are insured by the federal government and offer low- to moderate-income homebuyers lower down payment, debt-to-income and credit score requirements compared to conventional mortgages.

The minimum down payment is 3.5 percent and can include money received as a gift. Borrowers need a credit score of only 580, and those with credit scores between 500 and 579 are eligible for a loan-to-value ratio of 90 percent.

The minimum down payment is 3.5 percent and can include money received as a gift. Borrowers need a credit score of only 580, and those with credit scores between 500 and 579 are eligible for a loan-to-value ratio of 90 percent.

As long as the borrower lives in one unit, FHA loans can be used for multifamily properties up to four units. This has become popular for multigenerational families and rental units, Martin said.

Buyers Have Options

There are some downsides, including more costly mortgage insurance compared to conventional loans. FHA loans also assume a 1 percent payment of outstanding student loans, Martin said, even if the actual payment is less.

FHA loans also have limits that vary by county, making the product difficult to use in areas with high housing prices. Mortgage limits range from as low as $331,760 for a single-family home in New Haven or New London counties to $601,450 in Fairfield County.

First-time homebuyers in Connecticut do have other options. The Connecticut Housing Finance Authority has first-time homebuyer programs, as do the government-sponsored enterprises Fannie Mae and Freddie Mac.

In its annual report to congress released in June, the Federal Housing Finance Agency, which regulates the GSEs, said it had started working with the FHA last year to address overlaps between GSE and FHA loans.

The FHFA said in its report that the agencies were addressing the overlaps because the GSEs and FHA “were created to perform different roles in our housing finance system.” The GSEs are now also preparing to exit the conservatorship that they’ve been under since being taken over by the federal government in 2008.

“Our approach is to focus each program on fulfilling its distinct mission, while ensuring the secondary market continues to provide liquidity and access to credit,” the FHFA said in its report. “In order to responsibly exit the conservatorships, the [GSEs] must not stretch to serve borrowers who are better served by FHA. This is critical to not repeating the mistakes of the 2008 crisis.”

Concerns Eased

Concerns Eased

Last year, Connecticut saw a total of $1.83 billion in FHA lending, including $684.78 million in refinancing activity, more than two-and-a-half times the refinancing activity from 2018. FHA purchase activity rose to $1.15 billion from $1.08 billion in 2018.

The top FHA lender for mortgage companies in Connecticut in 2019 was Quicken Loans, and the top bank FHA lender was USAA Federal Savings Bank.

Guaranteed Rate was also among the top FHA lenders in 2019.

“FHA in general has always been a great product to serve low- to moderate-income borrowers, although there is no income limit, so borrowers of any income level can qualify for it, Martin said.

At the start of the economic crisis, Martin did see credit score requirements increase to 620, though that number has since eased back to 600. Other recent requirements have looked for borrowers to have at least two months’ worth of reserve payments after the down payment and closing costs.

“In an environment with employment loss and borrowers who don’t necessarily have a large equity position or a large reserves position to be able to weather however many months of disrupted income, it made sense that they tightened up a little bit and have since eased a little bit back,” Martin said.