With a 25-basis-point cut in the Federal Reserve’s benchmark interest rate expected in September, some local banks are eying improved profit margins. iStock illustration

An end to successive quarters of profit margin compression at Connecticut banks could be near, thanks to an expected September Federal Reserve rate cut that opens the door to reduced deposit expenses.

Federal Reserve Chair Jerome Powell indicate this week that the Fed will cut its benchmark interest rate in September, following the most recent meeting of the rate-setting Federal Open Market Committee.

The Fed’s benchmark interest rate has steadily climbed since 2022 and plateaued at between 5.25 percent and 5.50 percent starting in July of 2023.

For financial institutions, the current rate environment has depressed net interest margins – lenders have had to pay depositors more for the privilege of holding their money, and the higher rates have made most real estate developers and some business borrowers reluctant to take out large loans.

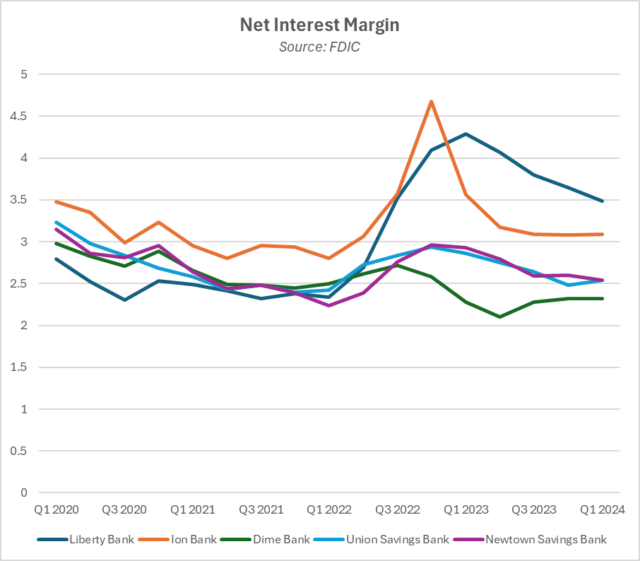

Among a select group of Connecticut stock and mutual banks analyzed by The Commercial Record for this story, the peak net interest margin of any one bank sat at 4.68 percent in the fourth quarter of 2022 while the lowest sat at 2.1 percent in Q2 of 2023,

The same could be said when looking at net interest income. For the majority of the banks analyzed, net interest income has been on the decline since 2023. Net interest income peaked at 4.34 percent among the group of banks while bottoming out at 1.98 percent in Q2 of 2023.

Ion Bank saw its net interest margin peak at 4.68 percent in the fourth quarter of 2022 but have since dropped to 3.09 percent according to FDIC data dating back to the start of 2020. Other Connecticut banks, like Union Savings Bank and Newtown Savings Bank, saw their NIM hit a floor of 2.54 percent.

Liberty Bank CFO Paul S. Young said the situation has made it tougher for consumers to access credit.

“High interest rates make borrowing money more expensive for consumers applying for mortgages, credit cards, auto loans, etc. and contributes to making it harder to get approved for loans,” he said. “Many lenders become more selective about who they make loans to because they fear that consumers may not be able to afford the higher payments. Consumers with savings to invest, earn higher interest payments on deposit products including savings accounts and certificates of deposit as banks compete for deposits to fund their lending activity.”

Expensive Deposits to Get Cheaper

Young has a positive outlook on the effect of potential rate cuts, noting that banks will be able to start cutting the interest they pay on some of their most expensive forms of deposits and offering more rewards to their customers.

“Once the Federal Reserve reduces their benchmark federal funds rate, floating rate loan payments will be reduced and many lending products tied to the rate will be priced lower helping more consumers qualify for loans,” Young said. “[Certificate of deposit] rates will eventually go down as interest rates are lowered but banks will be extremely cautious about losing these deposits. As a wave of CDs across the industry come up for renewal, successful banks will be creative in their product offerings and build full relationships to retain and attract new deposits. Consumers can expect these to include interest checking products with a sign-on bonus and subscription streaming services – Spotify, Netflix, etc. – as well as more attractive high yield savings accounts. Consumers with renewals coming due and additional funds to invest should lock in CDs soon before rates start to fall. Liberty Bank just introduced a 5.20% three-month CD which is almost 1 percent higher than any other Connecticut based bank and will be introducing a new high-yield savings account in the coming weeks.”

But reduced interest rates just won’t help bank customers. Young added that financial institutions will also see increased profitability.

Lower interest rates have historically been a stimulant for the economy as companies are more willing to hire employees, borrow money, invest in technology, and make capital purchases. As a result, lending activity increases and banks typically experience higher loan growth.

“Bank profitability is heavily based on the spread between the interest income they receive on loans and investments less the interest they need to pay on deposits and borrowings,” Young said. “The difference, or net interest income, has been compressed in the high interest environment due to the inverted yield curve that has been in place since October of 2022 and the battle for bank deposits that accelerated after the record bank failures in terms of asset size in 2023. Short-term rates are normally lower than long-term rates, but it is just the opposite when the yield curve is inverted. Since banks are normally borrowing short-term and price their lending products on longer term rates, many banks have been struggling in the ‘higher for longer’ interest rate environment. As inflation comes down closer to the Federal Reserve’s 2 percent target and interest rates are reduced, the yield curve should normalize helping to improve bank profitability as lending activity increases in a lower interest rate environment. Liberty Bank has had record earnings the past two years despite the high-rate environment and is positioned well for continued success in a lower rate environment.”

Aaron Jodka, national capital markets research director at commercial brokerage Colliers, said while the Fed’s signaled rate cut will be welcome, many borrowers will wish it had come sooner.

“The market’s been waiting anxiously for those Fed cuts,” Jodka said. “The market was expecting by this time, several rate cuts in 2024.”

While any cut might seem like some relief for consumers, Jodka said that a Fed rate cut this year could only be 25 basis points, which might not have a large impact.

Paul P. Schaus, managing partner at bank consultancy CCG Catalyst, said that even the effects of this rate cut will take time to filter down to banks and the wider economy, as the effects of Fed rate drops lag behind the central bank’s decisions.

“You’re not going to see all of a sudden the credit card company lower their interest rates,” Schaus stated. “Rates can go up and down, but the economic factors also affect how banks will pass [along] the rate decreases and who they pass [them to] because again, on the other side, you could have losses going up even with rates coming down.”