Minnesota developer hopes to tap into financing from a popular state program for its Enclave at Farmington River project. Image courtesy of Crown Equities

Rising interest rates and project costs threatened to bring major multifamily rental housing production virtually to a halt across Connecticut before a new program threw a lifeline to developers.

Since its creation in 2023, the Build for CT program has provided low-interest subordinate loans for 29 developments that are in the process of creating more than 3,200 apartments. Notable projects that have tapped into the program to complete their capital stacks include 240 apartments at Bridgeport’s Steelepoint Harbor project and 213 apartments at the former Ames department store headquarters in Rocky Hill.

The program is designed to address two urgent needs in Connecticut’s real estate market: creation of market-rate multifamily housing, and “missing middle” apartments reserved for households earning a maximum 60 to 120 percent of area median income. Projects with at least 50 housing units are eligible to participate.

“Deals weren’t penciling out,” said Vincent Bergin, business development officer for the Connecticut Housing Financing Agency. “Costs were up 20 or 30 percent and the banks were being a little more conservative.”

A partnership between the state Department of Housing and the CFDA, Build for CT was created in 2023 as rising costs and interest rates threatened to derail shovel-ready developments that have all of their permitting approvals in place.

Participation in the program comes with a set of caveats, designed to support the Lamont administration’s housing policy goals. Projects have to reserve at least 20 percent of units as income-restricted. They also aren’t eligible for low-income tax credits or some other state subsidies tied to affordable housing.

“The carrot for the low-interest rate loan is to have some middle-income restrictions, and that gives [developers] a cheap cost of capital and helps reduce their cost of capital on the overall project,” Bergin said.

The vast majority of participating projects are new construction, but adaptive reuse and historical rehabilitation projects also qualify, Bergin said.

Approximately a dozen projects are nearing completion. And more are joining the potential queue: Crown Equities, a Minnesota developer, indicated it will seek Build for CT financing for its proposed 258-unit Enclave at Farmington River project.

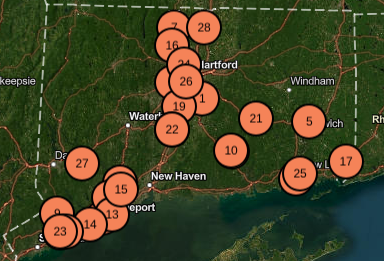

A map of housing developments receiving financing from the Build for CT project since its creation in 2023. Image courtesy of CFDA

Flexible Financing Terms – and Some Restrictions

The program’s funding comes from the state Department of Housing budget, subject to approval by the state Bond Commission. Projects qualify for loan up to $125,000 for each income-restricted unit.

The program has averaged approximately $50 million in annual funding awards, including construction loans and 20-year permanent loans, and offers fixed-rate loans in the 1-3 percent range. In January, CFDA awarded $7.4 million to projects totaling 231 homes.

In the absence of formal geographical guidelines, the program supports projects located in areas with job growth, transit-oriented sites, or other conditions that are favorable to multifamily development, Bergin said.

Likewise, the range of income restrictions varies from project to project, reflecting the estimated rents for market-rate units in the area.

In lieu of a formal competitive application process, CHFA staff work with developers that are in various stages of their projects, from early-stage permitting to, in some cases, projects that have already received construction financing, Bergin said. He anticipated the program will support up to 15 projects in a typical year, based upon its current funding level.

“There’s constant demand,” he said. “It’s just a function of the economy and different things: any type of disruption or uncertainty does cause change in the level of demand and bank financing.”